At first glance, the U.S. is winning fintech.

Yet, despite having the deepest capital markets and most iconic tech companies, launching a new fintech in the U.S. is excruciatingly hard.

We explore the structural barriers fintechs face in the U.S. and highlight how stablecoins enable a new generation of founders to build the next fintech giant.

Barriers To Progress

The combined burden of regulatory complexity and fragmented infrastructure creates the fundamental barrier to scaling a U.S. fintech.

State-by-State Compliance: Launching a payment service means applying for Money Transmitter Licenses (MTLs) in nearly every state. That’s 50+ applications, 50+ compliance programs, and waiting times of 3–24 months per license. Fintechs are additionally regulated at a federal level by various agencies: FinCEN, CFPB, Federal Reserve, OCC, and more. Each agency brings with it overlapping rules, expectations, and compliance burdens. From the outset, U.S. fintechs need the capital and time to navigate a complex, state-by-state, and federal licensing landscape.

Bank-by-Bank Integrations: The U.S. lacks a national open banking framework. Because of this, fintechs that require access to bank accounts must either negotiate relationships with each bank they work with or rely on aggregators like Plaid or Galileo, risking vendor locking. Banking as a service (BaaS) platforms can assist, but they must ensure that the fintech partnered with them has watertight compliance. This means fintechs must tailor KYC and AML programs with each BaaS/sponsor bank they work with, draining resources.

Combined, these obstacles result in fintechs requiring significant headcounts and capital. In essence, new fintech must navigate a walled garden of licenses and banking relationships in a game already mastered by its incumbents.

The U.S. is aware it has a problem.

For example, fintechs like Plaid, Visa, and Chime have lobbied for federal open-banking frameworks to lower bank integration friction for years. In this context, the Trump administration is also considering introducing regulatory reforms and leveraging technologies like stablecoins to boost its financial service industry.

Bridging The Innovation Divide

Fintechs operating in the U.S. and beyond are increasingly utilizing stablecoin rails.

Stablecoins are:

Global by design

Virtually free to send 24/7

Run on transparent, permissionless ledgers

Free of vendor locking

Increasingly accepted as a conventional means of payment

For fintech startups, this means faster time to market, lower capital requirements, and simplified compliance.

In the U.S., fintechs can partially or completely offload licensing responsibilities to partners like Bridge, Beam, and Paxos. This means that stablecoin-first fintechs can launch more quickly in the U.S., spend less time on compliance, and build useful products that delight customers without relying on a single vendor or banking relationship.

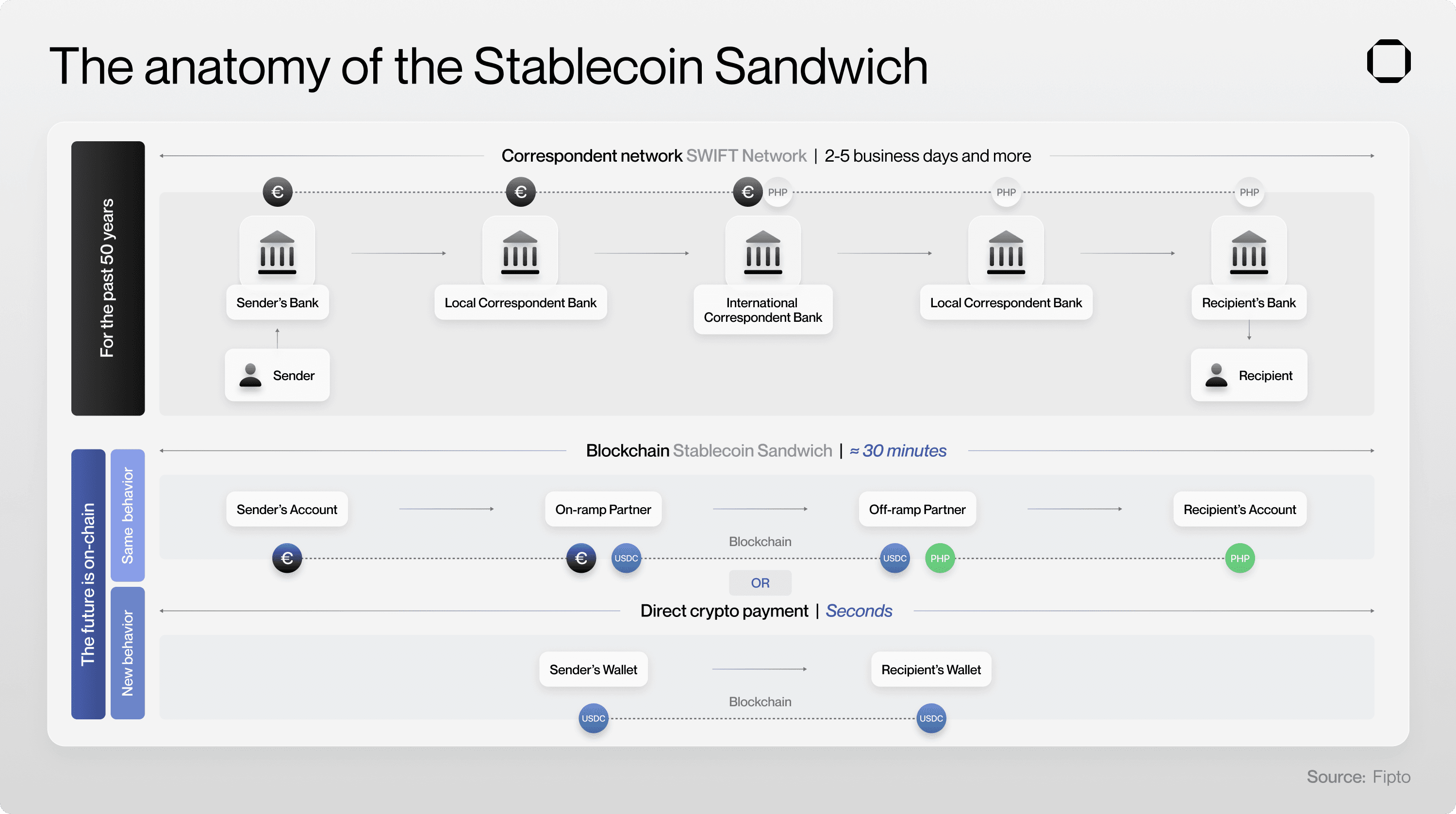

For instance, Sling Money, a stablecoin remittance application, requires only one registration to operate in the U.S. Similarly, Sphere, a stablecoin-to-fiat payment network, holds no money licenses and leverages relationships with licensed partners to facilitate the “stablecoin sandwich”, moving money across state lines and borders. This is possible as most stablecoin fintechs are “read-only”, meaning they don’t have custody over the transferred assets, accelerating money movement and simplifying compliance.

Last year alone, stablecoin-powered companies raised over $646M—more than any other crypto vertical. We're at an inflection point where stablecoins will begin to enable unprecedented fintech use cases, unleashing the next wave of financial innovation.

The rails are ready. It's time to build.

If you found this research valuable, follow us on 𝕏 to stay updated on our latest research and insights.